This finance solution is for UK window and door installers, glazing specialists and home improvement retailers that want to offer monthly payment options to customers. This is not personal finance for homeowners.

If you intend to offer finance to customers in the UK, it must be structured correctly and comply with Financial Conduct Authority regulations.

Offering customer finance does not mean becoming a lender. By working with a regulated credit broker, glazing businesses can introduce finance in a compliant and structured way.

For many window and door companies, customer finance helps reduce price resistance, increase average order value and improve cash flow stability. This guide explains how glazing businesses can offer finance safely and effectively.

Who This Guide Is For

This page is for home improvement businesses that want to offer finance to customers, including:

• uPVC window installers

• Aluminium window and door specialists

• Composite door retailers

• Bi fold and sliding door installers

• Conservatory and roof lantern installers

• Independent glazing contractors

• Bi fold door finance

• Composite door finance

• Conservatory finance

• Roof lantern finance

• Full house window replacement finance

If you operate in the glazing sector, offering finance enables customers to spread the cost of premium installations while protecting your margins.

Table of Contents

- What Does It Mean to Offer Window and Door Finance to customers?

- The Monthly Mindset and Why It Increases Sales when you offer Window and Door finance to customers

- When Should You Offer Finance to Customers?

- How Window and Door Finance Works

- Example of Window and Door Finance for Your Customers

- The Application and Payment Process

- What Products Can Be Covered?

- How Independent Firms Compete With National Brands

- Compliance and Risk Considerations

- Why Partner With Ideal4Finance?

- FAQs

- Get in Touch

What Does It Mean to Offer Window and Door Finance to customers?

Offering finance means giving customers the option to pay for their installation over time rather than paying the full amount upfront.

In most cases this involves:

• Consumer credit agreements

• Fixed monthly instalments

• A regulated lender providing the funds

• Your business acting as an introducer

Most glazing businesses do not lend money directly. Instead, they introduce customers to a regulated lender who manages the credit agreement and repayments.

Consumer Credit

Consumer credit is regulated lending to individuals. In the UK, it falls under the authority of the Financial Conduct Authority.

Instalments

Customers repay the lender in agreed monthly instalments over a fixed period.

Introducer Model

Most fireplace and stove businesses do not lend money directly. Instead, they introduce customers to a regulated lender. The lender handles the application, approval and repayment.

Regulated vs Unregulated Credit

If you offer regulated consumer credit without proper authorisation, you may breach Financial Conduct Authority rules. This is why many businesses choose to partner with an authorised provider.

The Monthly Mindset and Why It Increases Sales when you offer Window and Door finance to customers

Many homeowners accept that new windows or doors are necessary, but hesitation often appears when they see a large total cost.

Shifting the conversation towards monthly affordability changes the psychology of the sale. Instead of focusing on a significant upfront figure, the discussion becomes about how the project fits within a manageable household budget.

This approach often leads to:

• Higher quote to sale conversion rates

• Reduced decision delays

• Less reliance on discounting

• Greater uptake of upgrades and premium products

Premium aluminium frames, triple glazing and composite door upgrades feel far more accessible when presented in structured monthly terms.

When Should You Offer Finance to Customers?

Finance is most effective when introduced early in the sales process rather than after a customer raises affordability concerns.

This includes:

• Presenting a monthly payment alongside the full quotation

• Including finance within showroom and website pricing

• Positioning finance as a standard payment option

Introducing finance early helps customers assess affordability immediately and can reduce delays between quotation and confirmation.

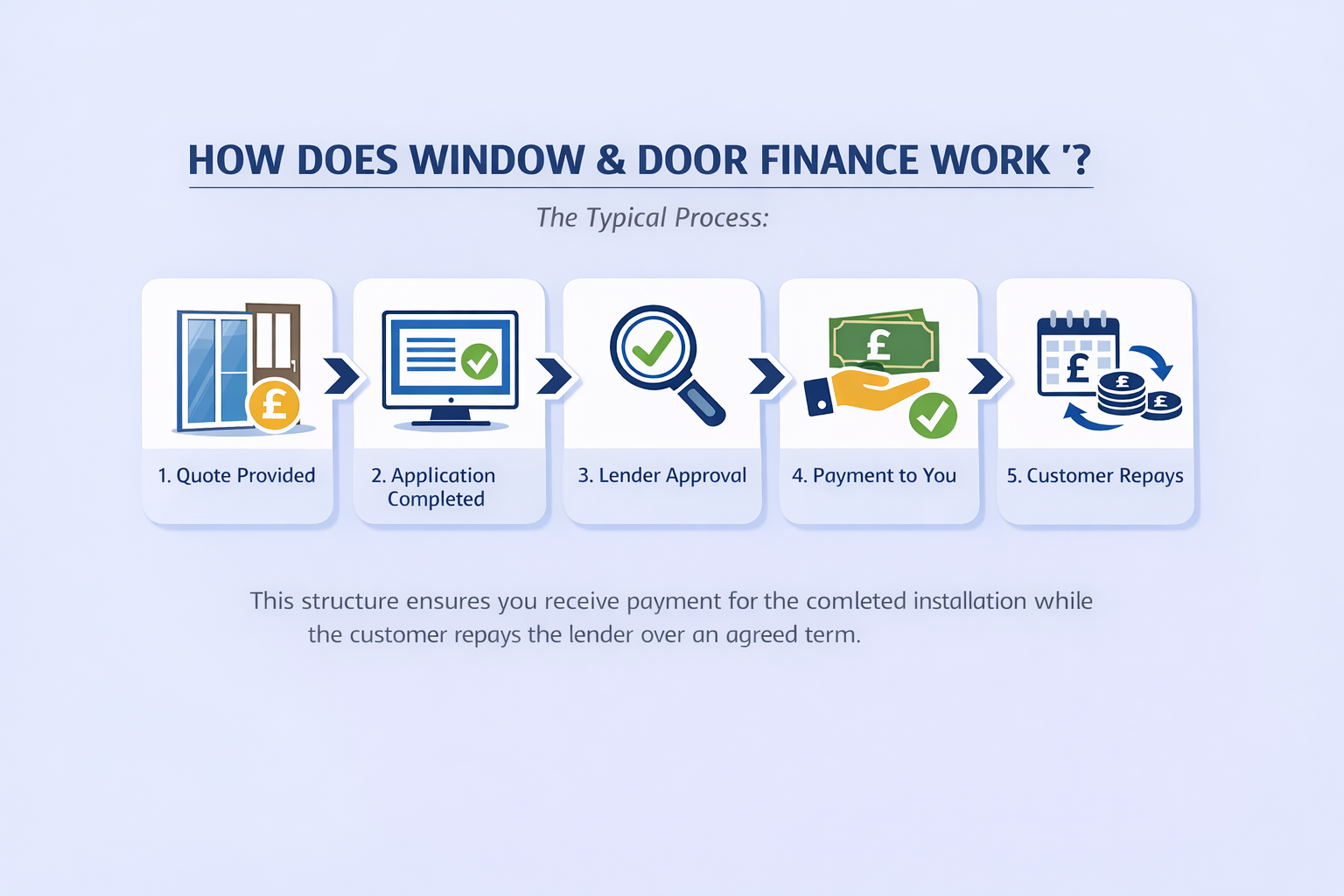

How Window and Door Finance Works

You do not lend the money yourself.

Instead, you partner with a regulated credit broker or finance provider.

The typical process is:

1 You provide a quotation that includes a finance option

2 The customer completes a finance application

3 The lender assesses the application

4 If approved, you are paid for the installation

5 The customer repays the lender in agreed monthly instalments

This structure ensures you receive payment for the completed installation while the customer repays the lender over an agreed term.

Example of Window and Door Finance for Your Customers

Window and door installations can vary depending on property size, specification and materials.

For example:

• Individual door replacements may range from £1,000 to £3,000

• Window packages may range from £3,000 to £10,000

• Full house replacements can exceed £15,000

Offering finance allows these costs to be spread over an agreed term.

Depending on the finance product, this may include:

• Fixed monthly repayments

• Optional deposits

• Flexible repayment terms

Presenting a monthly option alongside the full project cost helps customers make decisions more confidently.

The Application and Payment Process

The application process is designed to be simple and fully digital so it does not interrupt your sales process.

Once you agree the installation cost, the customer completes a short online application. The lender performs credit and affordability checks and provides a decision. If approved, the agreement is confirmed digitally.

After installation is completed and signed off, the lender pays your business directly. You are not responsible for collecting instalments and you do not carry long term repayment risk.

This protects your working capital and keeps your focus on fitting and operations rather than finance administration.

What Products Can Be Covered?

Most domestic glazing and home improvement installations can be funded through finance. This includes full house window replacements, bi fold door systems, composite doors, conservatories and roof lanterns.

Finance also allows you to bundle projects together. Customers may choose to upgrade glazing specifications, add additional doors or complete multiple rooms at once because the cost is spread across manageable monthly repayments.

This often results in higher quality installations and improved overall project value.

Why Do Customers Delay Window and Door Installations?

Customers often delay glazing projects even after receiving a quotation.

Common reasons include:

• Upfront cost concerns

• Comparing multiple installers

• Waiting for seasonal timing

• Uncertainty around total project cost

Offering finance provides a structured way to address these concerns and can help customers proceed without delaying the installation.

How Independent Firms Compete With National Brands

Large national window companies frequently promote finance heavily in their marketing.

Independent installers can compete effectively by offering structured monthly payment options through a regulated broker partnership.

By doing so, local glazing businesses can:

• Match national competitors on affordability

• Maintain personal service and local reputation

• Increase average project value

• Reduce lost sales due to upfront cost concerns

Offering finance levels the playing field without requiring a large administrative team or in house lending infrastructure.

Compliance and Risk Considerations

Introducing consumer credit in the UK is regulated activity. Finance promotions must be clear, transparent and compliant with Financial Conduct Authority standards.

When working with a regulated credit broker, the lending risk sits with the lender rather than your business. Once the installation is complete and approved, you are paid in full according to agreed terms.

This ensures your business can offer finance professionally while protecting both your reputation and cash flow.

Why Partner With Ideal4Finance?

Ideal4Finance supports UK installers and retailers who want to offer finance without becoming a lender.

Businesses choose Ideal4Finance because:

• The introducer model is straightforward

• Applications are managed securely online

• You receive payment after completion

• Compliance support is built into the process

• You can monitor applications through a dedicated portal

By positioning finance as a standard option rather than an afterthought, you can improve conversion rates and support customers in completing essential home upgrades sooner.

FAQs

Is it legal to offer window and door finance to customers in the UK?

Yes, but it is regulated. Businesses introducing credit must comply with Financial Conduct Authority requirements.

Do I need to be FCA authorised to offer window and door finance to customers?

In most cases, you will need appropriate permissions or must work with a regulated provider that structures the activity correctly.

Do customers expect finance when buying windows and doors?

Many customers now expect flexible payment options for higher value home improvements, particularly when replacing multiple windows or doors.

When do I get paid?

Once the installation is completed and signed off, payment is made directly to your business by the lender.

How do my sales increase once I offer Window and Door Finance to customers?

For many glazing companies, structured monthly options reduce price objections and increase overall conversion rates.

Get in Touch

Ready to offer finance to your fireplace and stove customers?

Call 020 3841 2817 or email sales@ideal4finance.com and our team will guide you through the process.

You can also visit https://ideal4finance.com/ to get started online.