This finance solution is for UK garden room companies, garden building specialists and outdoor living installers that want to offer monthly payment options to customers.

This is not personal finance for homeowners.

If you want to offer finance to your customers in the UK, you must ensure it is structured correctly and complies with Financial Conduct Authority regulations.

For many garden room businesses, offering finance can reduce price objections, increase average project value and improve cash flow. This guide explains how to introduce customer finance safely and effectively without becoming a lender yourself.

Who This Guide Is For

This page is for garden room businesses and outdoor building specialists, including:

- Garden room installers

- Garden office providers

- Modular garden building companies

- Outdoor studio installers

- Bespoke garden building contractors

- Landscaping companies offering premium structures

If you operate in this sector, offering finance allows customers to spread the cost of quality installations while protecting your margins.

Table of Contents

- What Does It Mean to Offer Garden Finance to customers?

- How Does Garden Room Finance Work?

- How Offering Garden Finance To Customers Helps You Win More Garden Room Projects

- How Our Introducer Model Works

- How to Stay Compliant and Protect Your Reputation

- Why Garden Room Businesses Choose Ideal4Finance

- How to Get Started

- FAQs

- Get in Touch

What Does It Mean to Offer Garden Finance to customers?

Offering finance means giving customers the option to pay for their garden room over time rather than paying the full amount upfront.

In most cases this involves:

- Consumer credit agreements

- Fixed monthly instalments

- A regulated lender providing the funds

- Your business acting as an introducer

Consumer Credit

Consumer credit refers to regulated lending to individuals. In the UK, it falls under the authority of the Financial Conduct Authority.

Instalments

Customers repay the lender in agreed monthly instalments over a fixed period.

Introducer Model

Most garden room businesses do not lend money directly. Instead, they introduce customers to a regulated lender. The lender manages the application, approval and repayment process.

Regulated vs Unregulated Credit

If you offer regulated consumer credit without proper authorisation, you may breach Financial Conduct Authority rules. This is why many businesses choose to partner with an authorised provider.

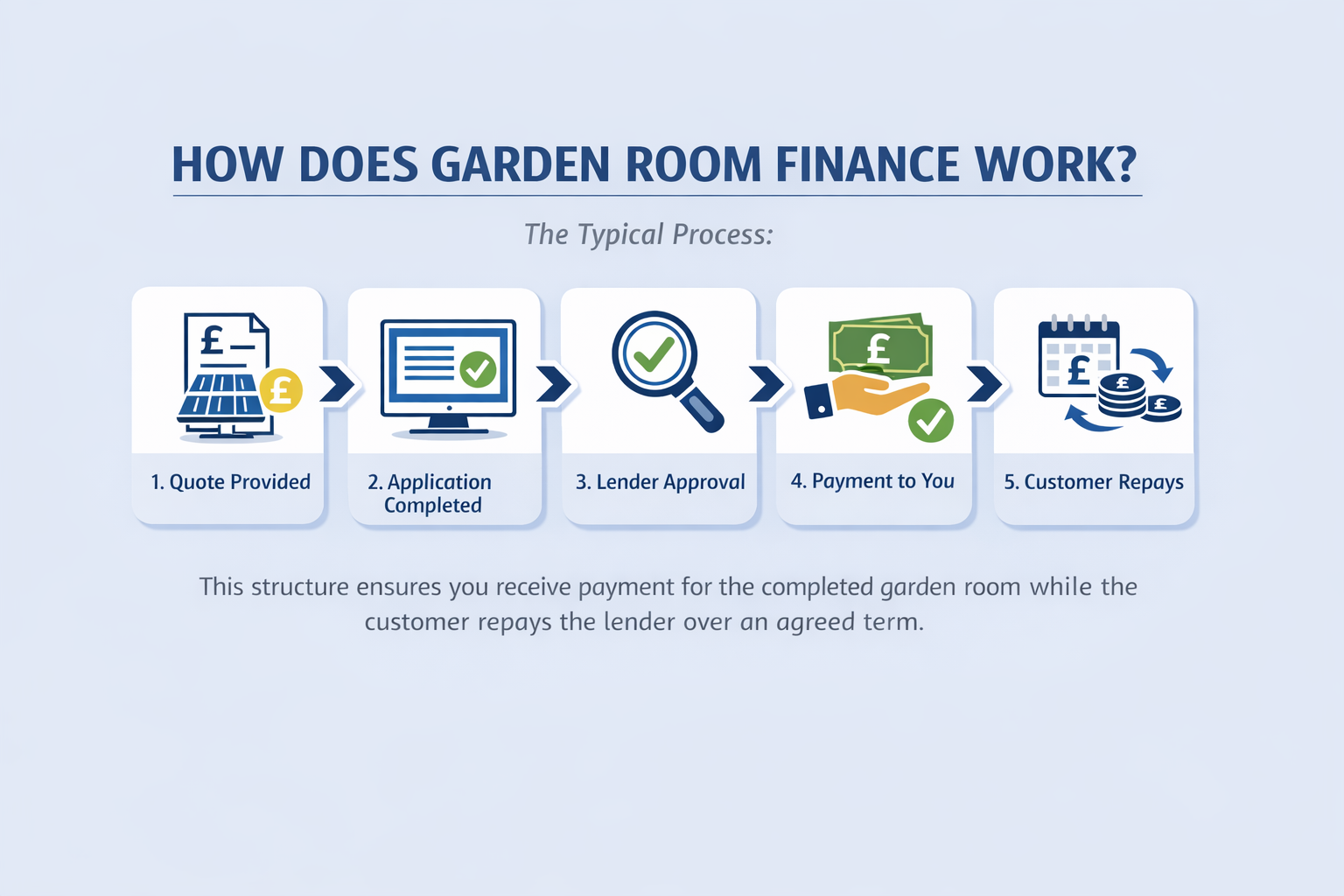

How Does Garden Room Finance Work?

You do not lend the money yourself.

Instead, you partner with a regulated credit broker or finance provider.

This allows your customers to spread the cost of their garden room, while you receive payment for the completed project.

The typical process works as follows:

- You provide a quotation that includes a finance option

- The customer completes a finance application

- The lender assesses the application

- If approved, you are paid for the installation

- The customer repays the lender in agreed monthly instalments

This structure ensures you receive payment for the completed garden room while the customer repays the lender over an agreed term.

How Offering Garden Finance To Customers Helps You Win More Garden Room Projects

Garden rooms are a considered purchase. Customers often compare options, delay decisions or reduce specifications based on budget concerns.

When you offer finance:

- More quotes are accepted

- Customers are less likely to delay

- You reduce pressure to discount

- Higher-spec finishes become more accessible

- Average order values can increase

Instead of focusing solely on the full project cost, conversations shift toward manageable monthly repayments.

This can be particularly valuable for:

- Garden offices

- Multi purpose garden studios

- Insulated yearly garden rooms

- Premium bespoke builds

When Should You Offer Finance to Garden Room Customers?

Many businesses only introduce finance when a customer raises concerns about price.

In practice, this can limit its effectiveness.

Finance is typically more effective when it is presented as part of your initial quotation.

This means:

• Showing a monthly payment option alongside the total project cost

• Positioning finance as a standard way to pay

• Allowing the customer to assess affordability early in the process

Introducing finance at the outset can reduce delays, minimise price objections and support faster decision making.

Example of Garden Room Finance for Your Customers

Garden room installations can vary significantly depending on size, specification and intended use.

For example:

• A standard garden office may range from £10,000 to £20,000

• A fully insulated, bespoke garden building may range from £20,000 to £40,000 or more

Offering finance allows this cost to be spread over an agreed term.

Depending on the finance product, this may include:

• Fixed monthly repayments

• Optional deposit contributions

• Different term lengths to suit customer budgets

Presenting a monthly option alongside the full project price allows customers to evaluate the project in a more practical and accessible way.

How Our Introducer Model Works

Offering finance does not need to be complicated.

Step 1 – You introduce finance as an option

You let the customer know monthly payments are available alongside the full project quotation.

Step 2 – The customer applies securely online

They complete an application directly with the lender.

Step 3 – The lender assesses eligibility

Credit checks and affordability assessments are handled by the lender.

Step 4 – You get paid

Once approved and the installation is completed, you receive payment.

Step 5 – The customer repays the lender

Repayments are made directly to the lender under agreed terms.

Why Do Customers Delay Garden Room Decisions?

Garden rooms are often discretionary purchases.

Customers may delay decisions due to:

• Upfront cost concerns

• Comparing multiple providers

• Uncertainty around budget allocation

• Timing of other home improvement projects

Offering structured finance can help address these barriers by providing a clear and manageable payment option.

This allows customers to move forward with confidence rather than postponing the project.

How to Stay Compliant and Protect Your Reputation

Introducing finance is a regulated activity.

That means you must adhere to:

- Clear communication of terms

- Transparent repayment information

- Proper documentation

- Responsible promotion

Working with a regulated provider helps ensure your finance offering aligns with Financial Conduct Authority expectations.

This protects both your customer and your reputation.

Why Garden Room Businesses Choose Ideal4Finance

Businesses choose Ideal4Finance because of:

- Introducer model simplicity

- Established panel of UK lenders

- Fast credit decisions

- Compliance support

Our approach is designed specifically for installers and home improvement businesses that want to offer finance without unnecessary complexity.

A dedicated marketing team can help create tailored materials, including website content and quotation wording.

Materials can also be reviewed before use to ensure they align with Financial Conduct Authority requirements.

Our approach is designed specifically for installers and home improvement businesses that want to offer finance without unnecessary complexity.

How to Get Started

Introducing finance into your garden room business is straightforward.

Our team will guide you through onboarding, explain how referrals work and ensure you understand your responsibilities.

Once set up, you can begin offering finance to customers who prefer to spread the cost.

Whether you are a sole trader or an established garden building company, finance can become a natural part of your sales process.

FAQs

Is garden room finance regulated in the UK?

Yes. If finance is offered to individuals, it typically falls under regulated consumer credit.

Do I need FCA authorisation to offer garden finance to customers?

In most cases, yes. Alternatively, you can work with an authorised provider who manages the regulated elements.

Can I offer staged payments instead?

Possibly, but structured instalment plans may fall under regulated credit rules. Always confirm your regulatory position.

Do I get paid upfront if a customer uses finance?

In most cases, yes.

Once the installation is complete and lender requirements are met, payment is made directly to your business.

The customer then repays the lender over time.

Does offering finance increase garden room sales?

For many installers, offering finance improves conversion rates by reducing the barrier of upfront cost.

It can also support higher specification builds and increased average order values.

Can finance be offered on bespoke garden room projects?

Yes.

Finance can typically be used for both standard and bespoke garden room installations, depending on the lender and project scope.

Is offering finance expensive for my business?

Costs vary depending on the type of finance product offered.

However, many businesses find that increased conversions and higher project values outweigh the associated costs.

Get in Touch

Ready to offer finance for your garden room projects?

Call 020 3841 2817 or email sales@ideal4finance.com and our team will guide you through the process.

You can also visit https://ideal4finance.com/ to get started online.