This finance solution is for UK boiler installers, heating engineers and plumbing businesses that want to offer monthly payment options to customers. This is not personal finance for homeowners.

If you want to offer finance to your customers in the UK, you must ensure it is structured correctly and complies with Financial Conduct Authority regulations.

For many boiler installers, offering finance can reduce price objections, increase sales and improve cash flow. This guide explains how heating and plumbing businesses can introduce customer finance safely and effectively, without becoming a lender themselves.

Who This Guide Is For

This page is for boiler and heating businesses wanting to offer finance to their customers, including:

• Boiler installers

• Heating engineers

• Gas Safe registered plumbers

• Central heating specialists

• HVAC contractors

• Bathroom and heating retailers

• Boiler replacement finance

• Central heating upgrade finance

• Air source heat pump finance

• Full heating system finance

• Boiler and controls package finance

If you operate in one of these sectors, offering finance helps customers spread the cost of quality heating installations while protecting your margins.

Table of Contents

- What does it mean to offer Boiler Finance to customers?

- How does Boiler Finance work?

- Do you need FCA Authorisation?

- When Should You Offer Finance to Your Customers?

- What are the Commercial Benefits to offer boiler finance to my customers?

- What Do Boiler Installers Often Get Wrong About Offering Finance?

- Is Offering Finance Risky for Boiler Installers?

- Does Offering Finance Affect Your Cash Flow?

- Does Offering Finance Increase Boiler Sales?

- FAQs

- Speak to Ideal4finance

What Does It Mean to Offer Boiler Finance to Customers?

Offering finance means giving customers the option to pay for their boiler installation over time instead of paying the full amount upfront.

In most cases this involves:

• Consumer credit agreements

• Fixed monthly instalments

• A regulated lender providing the funds

• Your business acting as an introducer

Consumer Credit

Consumer credit is regulated lending to individuals. In the UK, it falls under the authority of the Financial Conduct Authority.

Instalments

Customers repay the lender in agreed monthly instalments over a fixed period.

Introducer Model

Most boiler installers do not lend money directly. Instead, they introduce customers to a regulated lender. The lender handles the application, approval and repayment.

Regulated vs Unregulated Credit

If you offer regulated consumer credit without proper authorisation, you may breach Financial Conduct Authority rules. This is why many businesses choose to partner with an authorised provider.

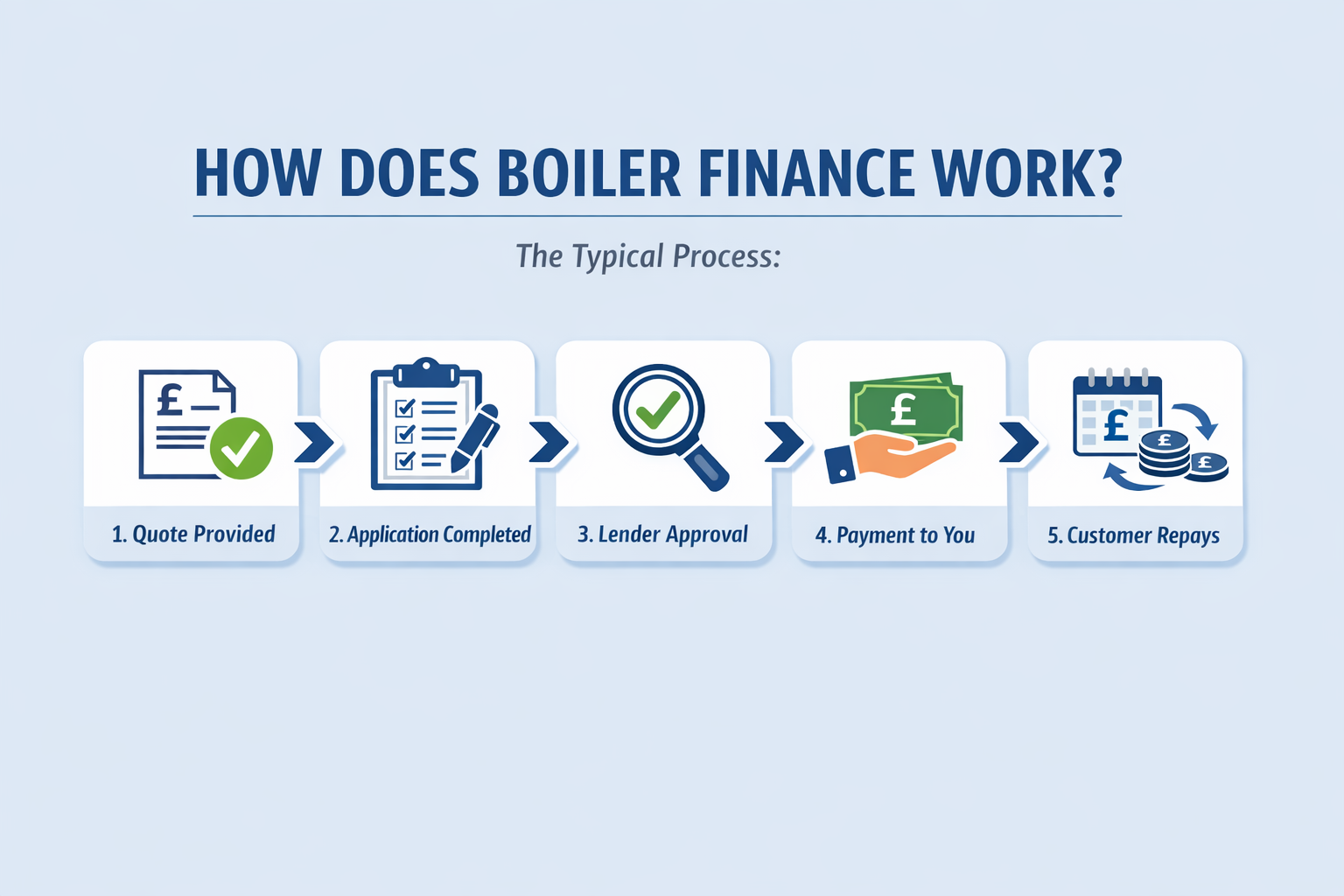

How Does Boiler Finance Work?

You do not lend the money yourself.

Instead, you partner with a regulated credit broker or finance provider.

The typical process is:

- You provide a quotation that includes a finance option.

- The customer completes a finance application.

- The lender assesses the application.

- If approved, you are paid for the installation.

- The customer repays the lender in agreed instalments.

This allows you to receive payment while giving your customer flexibility.

Offering Finance on a Boiler Installation

Instead of asking a customer to pay £5,000 upfront, you could offer:

- £0 deposit

- 12 months at 0% → £416.67 per month

This makes the installation significantly more accessible and often speeds up the decision making.

Do You Need FCA Authorisation?

In the UK, offering regulated consumer finance requires authorisation from the Financial Conduct Authority.

Most boiler installers operate as an Appointed Representative of an authorised credit broker. This allows you to offer finance without applying for your own direct FCA authorisation.

Working with an established broker helps ensure:

- Marketing materials are compliant

- Required disclosures are handled correctly

- Applications are processed appropriately

- Regulatory risk is reduced

Compliance should form part of your process from the outset.

When Should You Offer Finance to Your Customers?

Many installers only introduce finance when a customer raises concerns about price. In practice, this can limit its effectiveness.

Finance is typically more effective when it is included as part of your standard quotation process.

This means:

• Presenting a monthly payment option alongside the full installation cost

• Positioning finance as a normal way to pay

• Allowing the customer to choose what works for them

By introducing finance early, you reduce price objections and make higher value installations more accessible from the outset.

What are the Commercial Benefits to offer boiler finance to my customers?

Offering finance is not just about affordability for customers. It can strengthen your overall commercial performance.

Finance can help you:

- Increase sales without cutting prices

- Improve cash flow

- Compete with larger installers

- Position your business as established and professional

- Attract customers actively searching for monthly payment options

When introduced early in the sales conversation, finance becomes part of your standard quoting process rather than a last minute solution.

What Types of Boiler Finance Can You Offer?

Boiler installers can offer a range of finance options depending on the lender and commercial structure.

Common options include:

• Interest bearing finance (APR-based products)

• Interest free credit over a fixed term

• Deferred payment options

• Long-term repayment plans with lower monthly costs

Each option has different commercial considerations. For example, interest free credit may involve a higher subsidy, while interest bearing products can reduce upfront cost to your business.

A finance provider will explain which options are available and suitable for your business.

What Do Boiler Installers Often Get Wrong About Offering Finance?

Some businesses assume finance is complex or only suitable for larger companies.

Common misconceptions include:

• Thinking finance is difficult to set up

• Assuming customers will not use it

• Only mentioning it when a customer objects on price

• Worrying about taking on lending risk

In practice, finance is simply another payment option. When introduced early and presented clearly, it can become part of your standard sales process.

Is Offering Finance Risky for Boiler Installers?

When structured correctly, the risk to your business is limited.

You are not the lender. The finance provider is responsible for:

• Credit checks

• Approval decisions

• Customer repayments

If a customer does not repay, this does not become your liability, provided the agreement has been introduced compliantly.

Does Offering Finance Affect Your Cash Flow?

In most cases, offering finance can improve cash flow rather than restrict it.

Once the installation is complete and lender requirements are met, payment is made to your business by the finance provider.

The customer then repays the lender directly.

This means:

• You are not waiting for staged payments

• You are not collecting instalments

• You are paid in line with agreed terms

Does Offering Finance Increase Boiler Sales?

In many cases, yes.

Customers often make decisions based on affordability rather than total cost. By offering a monthly payment option, you allow customers to proceed with installations that might otherwise be delayed or reduced in scope.

For boiler installers, this can result in:

• Higher conversion rates

• Increased average job values

• More upgrades and system improvements being accepted

Learn How to Offer Plumbing and Heating Finance to Customers

If you want to understand how to introduce finance into your business in a compliant way, read our full guide:

Offer Plumbing and Heating Finance to Customers – Guide for UK Installers

This explains the process, regulatory requirements and how to get started.

FAQs

How to offer boiler finance to customers?

Yes, boiler installers in the UK can offer finance, provided they do so compliantly.

You will either need direct authorisation from the FCA or operate as an Appointed Representative of an authorised credit broker. Most installers choose the Appointed Representative route to avoid managing regulatory requirements themselves.

Will offering boiler finance to customers slow down my payment?

No. In most cases, once the installation is complete and lender requirements are satisfied, you are paid by the finance provider.

The customer then repays the lender over time. You are not waiting for monthly instalments.

What is the best source of finance for a small business?

For most small boiler installation businesses, partnering with a regulated credit broker is the most practical option.

A broker provides access to lenders, manages compliance obligations and supports the application process, allowing you to focus on running your business.

Can you offer boiler finance to customers for installations?

Yes, boiler installations are commonly financed in the UK.

Finance can cover the cost of the boiler, labour and associated installation work. If approved, the customer repays the lender over an agreed term.

Is boiler finance hard to get?

Approval depends on the customer’s individual circumstances and the lender’s criteria.

Many customers are eligible, but not every application will be approved. The lender assesses affordability and suitability as part of the process.

Is offering finance expensive for my business?

Costs vary depending on the type of finance offered. For example, interest free credit may involve a higher subsidy than interest bearing options.

However, many installers find that improved conversion rates and higher job values outweigh the cost.

A finance partner can explain the commercial structure clearly before you proceed.

Do I get paid upfront if my customer uses finance?

In most cases, yes.

Once the installation is complete and the lender process is complete, payment is released to your business.

You are not paid in instalments.

How long does it take to set up finance for my business?

Setup time depends on the provider and your business structure.

For installers operating as an Appointed Representative, the process is typically straightforward and quicker than applying for direct FCA authorisation.

Can I offer finance on all types of heating work?

In most cases, yes.

Finance can be used for:

• Boiler installations

• Central heating upgrades

• Air source heat pumps

• Full heating systems

• Controls and related work

Can I promote finance on my website and quotes?

Yes, but it must be done compliantly.

Financial promotions are regulated, so marketing materials must include the correct disclosures and follow FCA guidelines.

Working with an authorised broker helps ensure this is handled correctly by a Marketing team.

Speak to Ideal4Finance

If you are a boiler installer considering offering finance, Ideal4Finance can explain how the process works and whether it is suitable for your business.

You can call 020 3841 2817 or email sales@ideal4finance.com and our team will guide you through the process.